Introduction

If you think Financial Statements are just for the accounting department, think again. As a Physical and Infrastructure Asset Manager, these documents are among the most powerful tools in your arsenal. They are the language you use to communicate the value of your assets, to justify critical investments, and to demonstrate the financial consequences of operational decisions. Whether you're making a case for a new bridge, a fleet upgrade, or an expanded maintenance program, your argument will live or die by the numbers in these reports.

This isn't about becoming an accountant. It's about learning to read the story that these statements tell about the assets under your stewardship. It’s about connecting the physical reality of your infrastructure—its condition, its performance, its risks—to the financial reality of the organization. Understanding this connection is what separates a caretaker from a strategic leader in asset management.

The Three Pillars of Financial Reporting

At the heart of financial reporting are three core documents that work together to provide a comprehensive view of an organization's financial health. Think of them as different camera angles on the same subject. One gives you a static, wide shot, another shows the action over a period, and the third follows the money.

📊 View Diagram: How the Three Financial Statements Connect

Understanding how these statements influence each other is the first step. An action recorded on one statement will almost always have a corresponding effect on at least one of the others.

The Balance Sheet: A Snapshot in Time

The Balance Sheet is exactly what it sounds like: a statement that must balance. It presents a snapshot of what an organization owns (Assets) and what it owes (Liabilities) at a single point in time. The difference between these two is the organization's net worth, or Equity.

Assets = Liabilities + Equity

For an asset manager, the "Assets" section is where the action is. This is where the physical infrastructure you manage is financially represented. Assets are typically split into two categories:

- Current Assets: Cash and other resources expected to be converted to cash or used up within one year.

- Non-Current Assets: Long-term assets not expected to be converted to cash within a year. This is the home of Property, Plant, and Equipment (PP&E)—your buildings, pipelines, vehicle fleets, and power grids.

When your organization acquires a new piece of heavy machinery or completes construction on a new facility, its value is added to the Non-Current Assets on the balance sheet. But that value doesn't stay static. Over time, as an asset is used, it wears out. This gradual reduction in value is a real business expense, and it's recognized through a process called Depreciation. Each year, a portion of the asset's cost is expensed, and its book value on the balance sheet decreases.

A related concept, often seen with intangible assets like software licenses or land-use rights, is Amortization. While the mechanics are similar, depreciation applies to tangible, physical assets, and amortization applies to intangible ones.

The Income Statement: Performance Over a Period

If the balance sheet is a photo, the Income Statement (also known as the Profit & Loss or P&L) is a video. It shows an organization's financial performance over a specific period, like a quarter or a year. Its formula is simple:

Revenues - Expenses = Net Income

As an asset manager, you have a significant impact on the "Expenses" side of this equation. This is where the costs associated with acquiring, operating, and maintaining your assets are recorded. These costs fall into two critical categories that you must understand: Capital Expenditure (CapEx) and Operating Expenditure (OpEx).

The distinction is fundamental.

- CapEx is an investment. When you spend money to buy a new generator or perform a major overhaul that extends a pipeline's life, that's CapEx. The cash is spent, but the cost isn't recognized on the income statement all at once. Instead, the asset is added to the balance sheet, and its cost is spread out over its useful life via depreciation.

- OpEx is a running cost. The money you spend on routine inspections, preventative maintenance, fuel, and minor repairs is OpEx. These expenses are recorded on the income statement in the period they occur, directly reducing the net income for that period.

The Strategic Choice: CapEx vs. OpEx

Deciding whether to classify a major work order as a life-extending capital upgrade (CapEx) or a large-scale repair (OpEx) is a critical strategic decision. Classifying it as OpEx will hit your current period's profitability hard. Classifying it as CapEx improves short-term profit but adds to the long-term asset base and future depreciation. This decision directly shapes the financial narrative of your asset portfolio and requires careful judgment.

The Statement of Cash Flows: Following the Money

The income statement can be misleading because it includes non-cash expenses like depreciation. An organization can show a healthy net income but still run out of cash. The Statement of Cash Flows corrects for this by tracking the actual movement of cash over a period. It's broken into three activities:

- Cash from Operating Activities: The cash generated or spent by normal business operations. This is where you see the cash paid for OpEx-related activities like maintenance and repairs.

- Cash from Investing Activities: The cash used for investments. For an asset manager, this is the most important section. When you buy a new fleet of trucks (CapEx), the cash outflow appears here. When you sell an old building, the cash inflow appears here. This section is the pure cash reflection of your capital investment strategy.

- Cash from Financing Activities: The cash flow between a company and its owners and creditors (e.g., issuing stock, paying dividends, taking out loans).

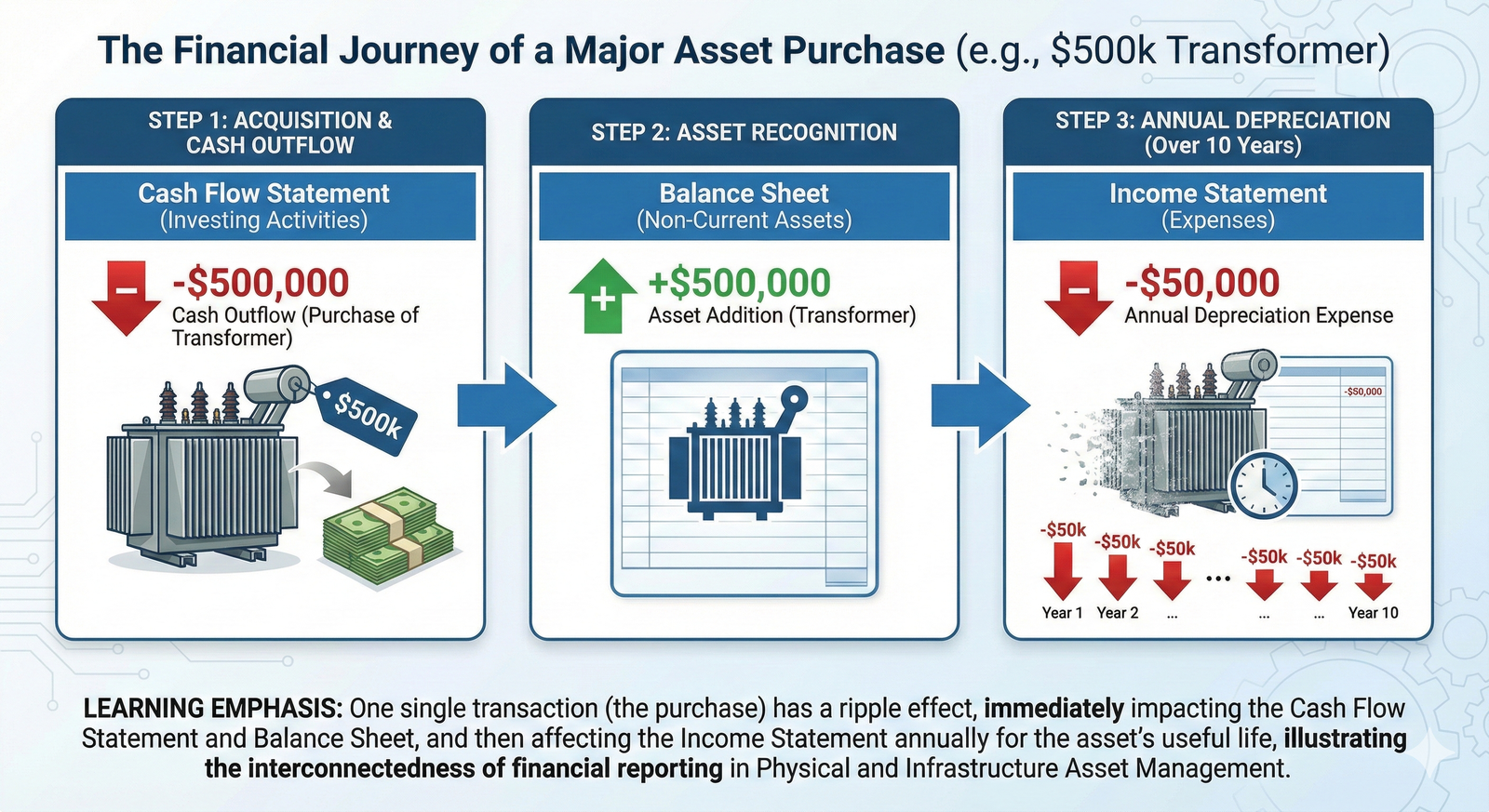

Let's trace a single transaction. Imagine your utility company buys a new transformer for $500,000 cash.

- Statement of Cash Flows: Shows a $500,000 cash outflow under "Investing Activities." The company's total cash is immediately reduced.

- Balance Sheet: "Cash" (a current asset) decreases by $500,000, but "Property, Plant, & Equipment" (a non-current asset) increases by $500,000. The balance sheet remains in balance.

- Income Statement: In the first year, there is no immediate impact on the income statement from the purchase itself. However, at the end of the period, the depreciation expense for the transformer (e.g., $50,000 if it has a 10-year life) will be recorded. This expense reduces net income.

Looking to the Future: From Static Reports to Dynamic Insights

Historically, financial reporting has been a backward-looking exercise, based on fixed depreciation schedules and periodic data entry. But this is changing. The rise of the "digital twin"—a virtual model of a physical asset, updated in real-time with sensor data—is poised to revolutionize this space.

Imagine a future where depreciation isn't calculated on a straight-line basis over 20 years. Instead, it's calculated dynamically based on real-time data from a bridge's strain gauges or a pipeline's corrosion sensors. An asset that is used more heavily or in harsher conditions would depreciate faster, providing a much truer financial picture of its value. As an asset manager, your ability to integrate this kind of operational data with financial reporting will be a key skill, allowing you to provide unprecedented insight into the true cost and value of your infrastructure portfolio.

Closing

We've covered the purpose and structure of the three core financial statements: the balance sheet, the income statement, and the statement of cash flows. More than just definitions, you can now see how these documents are deeply intertwined with the daily realities of managing physical and infrastructure assets. They are not passive records but active tools for decision-making.

You can now identify how your key activities, from a major capital acquisition to a routine maintenance schedule, leave their fingerprints on these financial reports. Understanding the difference between CapEx and OpEx and knowing how depreciation impacts both the balance sheet and income statement are foundational concepts. By mastering this language of finance, you are better equipped to advocate for your assets, justify your budgets, and demonstrate the value you create for your organization.

Learning Outcomes

In this reading, you have developed the skills to interpret the financial narrative of your asset portfolio. You can now:

- Explain the distinct purpose of the balance sheet (a snapshot of value), the income statement (a report of performance), and the cash flow statement (a record of money movement), and describe how they interrelate.

- Trace the financial impact of key asset management decisions, such as acquiring new infrastructure (Capital Expenditure) or performing routine maintenance (Operating Expenditure), across the three statements.

- Define and differentiate between the core financial concepts of Financial Statements, Depreciation, Amortization, Capital Expenditure (CapEx), and Operating Expenditure (OpEx) as they apply to physical assets.

Assess Yourself

❓ Knowledge Check

Test your understanding of the key concepts from this section.

Next Steps

You've now established a solid foundation for understanding the financial language that underpins strategic asset management. Well done. Please navigate back to the course to continue your learning journey.