Introduction

Imagine you're the asset manager for a major water utility. You have two proposals for a critical new pumping station. Proposal A has a significantly lower initial construction cost, which looks great for this year's budget. Proposal B is more expensive upfront but uses higher-grade pumps and corrosion-resistant pipes, promising lower energy consumption and fewer maintenance call-outs over its 30-year design life.

Which do you choose?

If your decision is based solely on the initial price tag, you might be setting your organization up for decades of escalating costs and operational headaches. This is where the discipline of Whole-Life Costing becomes not just useful, but essential. It provides a structured framework for looking beyond the immediate capital outlay to understand the full, long-term financial picture of an asset. It's about making a smart investment, not just a cheap purchase. This way of thinking is fundamental to responsible and sustainable asset management.

The Shift in Perspective: From Price to Total Cost

For a long time, particularly in public sector procurement, the "lowest bid wins" mentality was standard practice. This approach, focused entirely on minimizing the initial purchase price, often led to unintended and costly consequences. We've all seen the results: public buildings that are expensive to heat, roads that require constant repair, and equipment that fails prematurely. These are the ghosts of short-sighted, capital-focused decisions.

The realization that the purchase price is often just the tip of the iceberg led to the development of Whole-Life Costing. It's a strategic shift from focusing on the initial spend to understanding the total economic impact of owning and operating an asset.

WLC and Sustainable Investment

Whole-Life Costing is the financial backbone of sustainable asset management. By forcing you to consider long-term energy use, maintenance needs, and disposal impacts, it naturally guides decisions toward more durable, efficient, and environmentally responsible solutions. A sustainable choice is almost always one with a lower whole-life cost, even if the initial price is higher.

This approach is not just about saving money in the long run; it's about ensuring value and service delivery. When you manage public infrastructure—a water network, a power grid, a transit system—your primary responsibility is to provide a reliable service for decades to come. WLC aligns financial planning with this long-term service obligation.

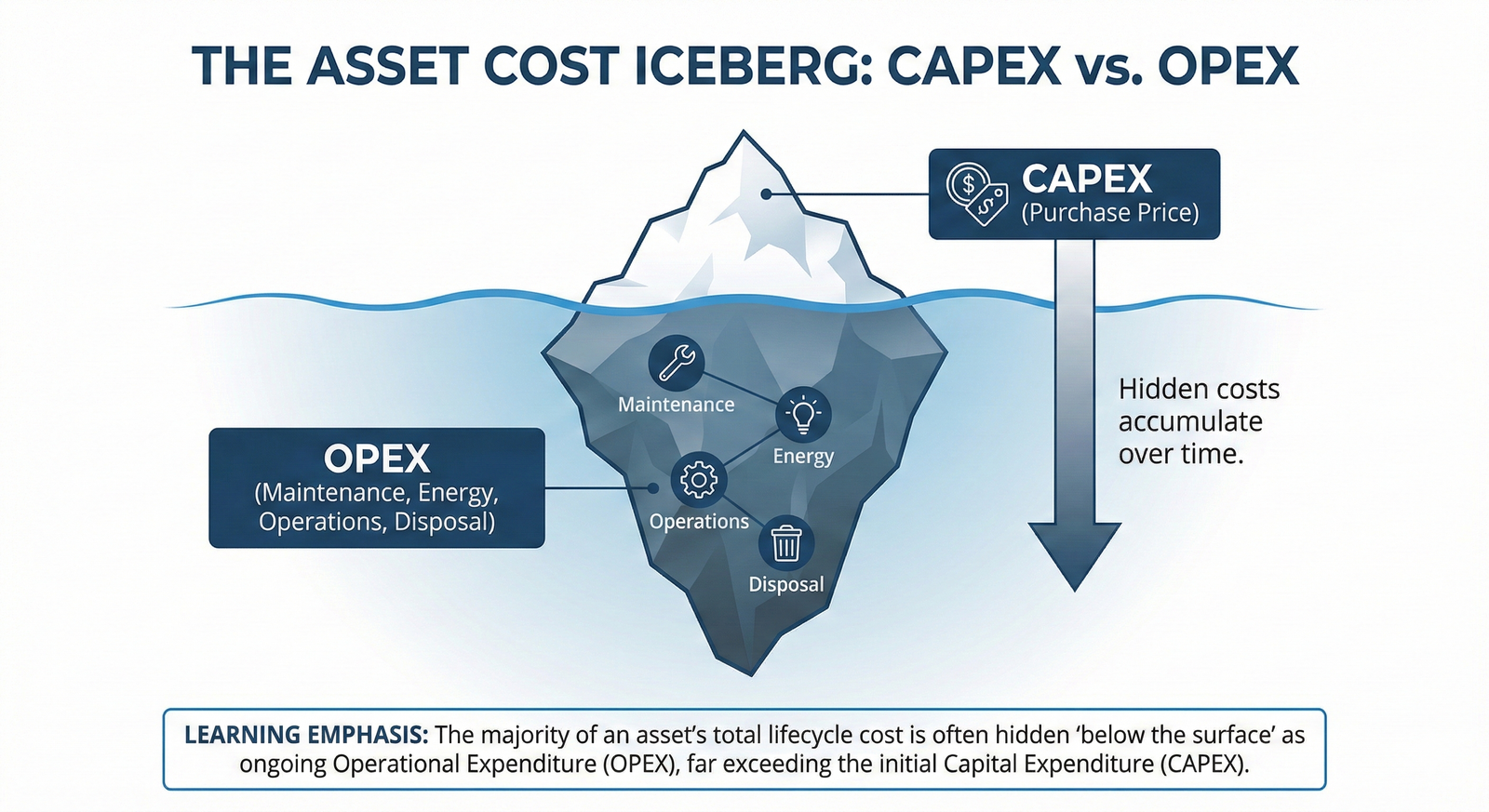

The Two Sides of the Cost Ledger: CAPEX and OPEX

To perform a proper WLC analysis, you first need to get comfortable with two fundamental categories of expenditure. Every cost associated with an asset will fall into one of these two buckets.

First, you have Capital Expenditure (CAPEX). This is the money you spend to get the asset. Think of the major, one-off investments: * The purchase price of a new fleet of service vehicles. * The construction cost of a new wastewater treatment plant. * The cost of a major software system and its initial implementation.

On the other side of the ledger is Operational Expenditure (OPEX). This is the money you spend to run the asset. These are the recurring, everyday costs: * Fuel, insurance, and routine oil changes for the service vehicles. * Electricity, chemicals, and operator salaries for the treatment plant. * Annual licensing fees and technical support for the software system.

The core tension in many asset decisions is the trade-off between CAPEX and OPEX. A low-CAPEX option might come with high-OPEX baggage. For example, a cheaper, less efficient HVAC system (low CAPEX) will result in higher monthly energy bills (high OPEX) for the next 20 years. Conversely, investing more upfront in a high-efficiency system (high CAPEX) can generate significant OPEX savings that pay back the initial investment many times over. WLC is the tool that allows you to quantify this trade-off and find the optimal balance.

A closely related concept you'll frequently encounter is Total Cost of Ownership (TCO). For most practical purposes in asset management, TCO and WLC refer to the same holistic approach of analyzing costs over the asset's life.

Assembling the Puzzle: The Components of a WLC Analysis

A robust WLC analysis is more than just a back-of-the-envelope calculation. It's a structured process that involves several key stages and cost components.

📊 View Diagram: The Whole-Life Costing Analysis Process

As the diagram shows, the analysis requires you to forecast several distinct types of costs over the asset's entire life cycle:

- Acquisition Costs: This is your CAPEX. It includes the purchase price, but also transportation, installation, and commissioning costs. For a complex asset like a new manufacturing line, this could involve significant engineering and integration work.

- Operating Costs: This is the primary component of your OPEX. It includes energy consumption, fuel, water, and any other utilities or consumables required to run the asset. It also includes the labor costs for the operators who run the equipment.

- Maintenance Costs: A critical and often underestimated part of OPEX. This includes costs for planned preventive maintenance (inspections, lubrication, filter changes) and a budget for unplanned corrective maintenance (breakdowns and repairs). This requires good historical data or reliable manufacturer estimates.

- Disposal Costs: Every asset eventually reaches the end of its useful life. The cost to decommission, remove, and dispose of the asset must be included. This can be a significant cost, especially if there are environmental regulations to follow, such as with the disposal of assets containing hazardous materials. In some cases, an asset might have a residual or salvage value, which would be a negative cost (a credit) in your analysis.

The Time Machine: Making Fair Financial Comparisons

Here's a question: Is a $10,000 repair bill ten years from now the same as a $10,000 bill today?

Absolutely not. Money has a time value. A dollar in your hand today is worth more than the promise of a dollar in the future. This is because of inflation (it will buy less in the future) and opportunity cost (you could invest that dollar today and have it grow). To compare costs that occur at different points in time, we need a way to bring them all to a common baseline.

This is done using a technique called Discounted Cash Flow (DCF). The formula discounts future costs using a "discount rate," which represents the rate of inflation and opportunity cost.

The result of this DCF analysis for all the costs over the asset's life is a single number called the Net Present Value (NPV). By calculating the NPV for each asset alternative, you can finally make a fair comparison. The option with the lowest NPV is the most economically favorable choice over the long term.

The Critical Role of the Discount Rate

The discount rate you choose can dramatically alter the outcome of a WLC analysis. A high discount rate makes future costs seem smaller, favoring options with low upfront CAPEX. A low discount rate gives more weight to future OPEX, favoring options that are built to last. Choosing and justifying the discount rate is one of the most critical and scrutinized steps in any WLC study.

Let's look at a simplified example. We'll use the water pump scenario from the introduction.

20-Year Cost Projections for Water Pump Alternatives

| Cost Item | Pump A (Standard Efficiency) | Pump B (High Efficiency) |

|---|---|---|

| Acquisition Cost (CAPEX) | 25000 | 60000 |

| Annual Energy Cost | 8500 | 5000 |

| Annual Maintenance Cost | 3000 | 1500 |

| 20-Year Disposal Cost | 2500 | 2800 |

Without a WLC analysis, Pump A looks like the winner with its lower acquisition cost. But when we project the OPEX over 20 years and discount those future costs to find the NPV, a different story emerges. The higher annual energy and maintenance costs of Pump A add up year after year. Even when discounted, the NPV of Pump A's total cost will likely be significantly higher than that of Pump B. The WLC analysis proves that the higher initial investment in Pump B is the more financially prudent decision.

Navigating the Fog: Real-World Challenges in WLC

While the principles of WLC are straightforward, applying them in practice is fraught with challenges. A perfect analysis is impossible; the goal is to create a well-reasoned and defensible one.

- The Data Dilemma: The single biggest challenge is the quality of your data. The analysis is only as good as the cost estimates you feed into it. Predicting maintenance costs 15 years from now is an exercise in educated guesswork. This is where historical data from your asset register and CMMS (Computerized Maintenance Management System) becomes invaluable. Without it, you're heavily reliant on manufacturer data, which may be optimistic.

- Defining the "Whole Life": What is the appropriate analysis period? For a laptop, it might be 5 years. For a bridge, it could be 100 years. This choice has a huge impact on the outcome and must be aligned with the asset's expected service life.

- Quantifying the Intangibles: How do you put a price on reliability? The cost of a pump failing isn't just the repair bill; it's the cost of service interruption, potential regulatory fines, and damage to your organization's reputation. While difficult, advanced WLC models attempt to quantify these risks and "hidden" costs.

- A Glimpse into the Future: The world changes. Energy prices fluctuate, new technologies emerge, and regulations are updated. A WLC analysis is a snapshot based on today's assumptions. This is why a sensitivity analysis is a crucial final step. You should re-run the numbers with different assumptions (e.g., "What if energy prices double?") to see how sensitive your conclusion is to these variables.

Looking ahead, the rise of the Internet of Things (IoT) and predictive analytics is set to revolutionize WLC. Instead of estimating future maintenance costs, we can now install sensors that monitor an asset's health in real-time.

This data allows us to move from a preventive maintenance schedule ("change the oil every 500 hours") to a predictive one ("the sensor data indicates bearing wear; failure is likely within 80 hours"). This ability to forecast costs with much greater accuracy will make WLC an even more powerful and reliable tool for asset managers.

Closing

Returning to our water utility, the choice is now clear. While the upfront cost of Proposal A was tempting, a thorough Whole-Life Costing analysis reveals it to be a false economy. The long-term burden of higher energy and maintenance costs—the OPEX—far outweighs the initial CAPEX savings. The sustainable and fiscally responsible choice is Proposal B. It represents a better investment of public funds and a greater certainty of reliable service for the community.

Whole-Life Costing is more than an accounting technique; it's a strategic mindset. It forces you and your organization to think beyond the immediate budget cycle and consider the long-term consequences of your decisions. It provides a rational, defensible framework for balancing CAPEX and OPEX, navigating complex trade-offs, and ultimately, delivering the best possible value over the entire life of your critical assets. Mastering this practice is a hallmark of a mature and effective asset management professional.

Learning Outcomes

In this reading, you have explored the principles and practices that underpin modern asset investment decisions. You can now:

- Explain why Whole-Life Costing is a critical tool for making sustainable and economically sound investment choices for physical and infrastructure assets.

- Clearly distinguish between the upfront investment in an asset (Capital Expenditure) and the ongoing costs to run it (Operational Expenditure).

- Identify the essential cost components—acquisition, operation, maintenance, and disposal—that form a complete Whole-Life Costing analysis, and recognize the challenges involved in gathering data and making long-term forecasts.

You have also been introduced to the key financial concepts, including Total Cost of Ownership, Discounted Cash Flow, and Net Present Value, that allow for fair, "apples-to-apples" comparisons between different asset options.

Assess Yourself

Check your understanding of the key concepts from this reading.

❓ Knowledge Check

Test your understanding of the key concepts from this section.

Next Steps

You have now completed this reading on the fundamentals of Whole-Life Costing. This is a foundational concept that you will see applied in future case studies and analyses. Please navigate back to the course page to continue to the next activity.